Residual Profit Split

Split residual profit defensibly when value creation is shared.

Apply the residual profit split method where parties make unique and valuable contributions — with rigorous routine return benchmarking, residual identification, and value-driver allocation in one workflow.

Defensible Profit Splits, Grounded in Substance

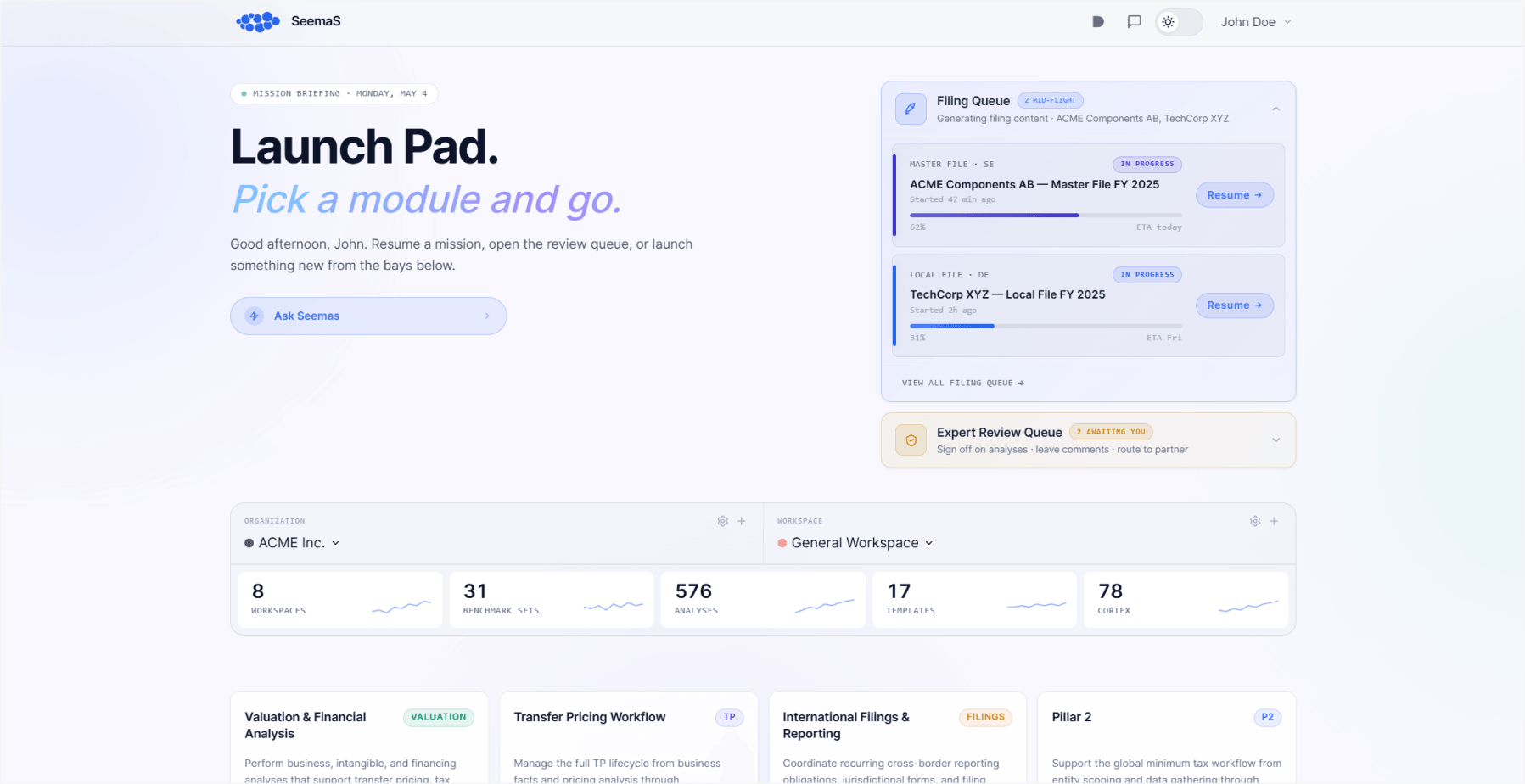

Begin in a centralized workspace that surfaces your active projects, pending requests, and priority entities, so your team can move from intake to documentation without switching between disconnected tools.

Streamline Workflows

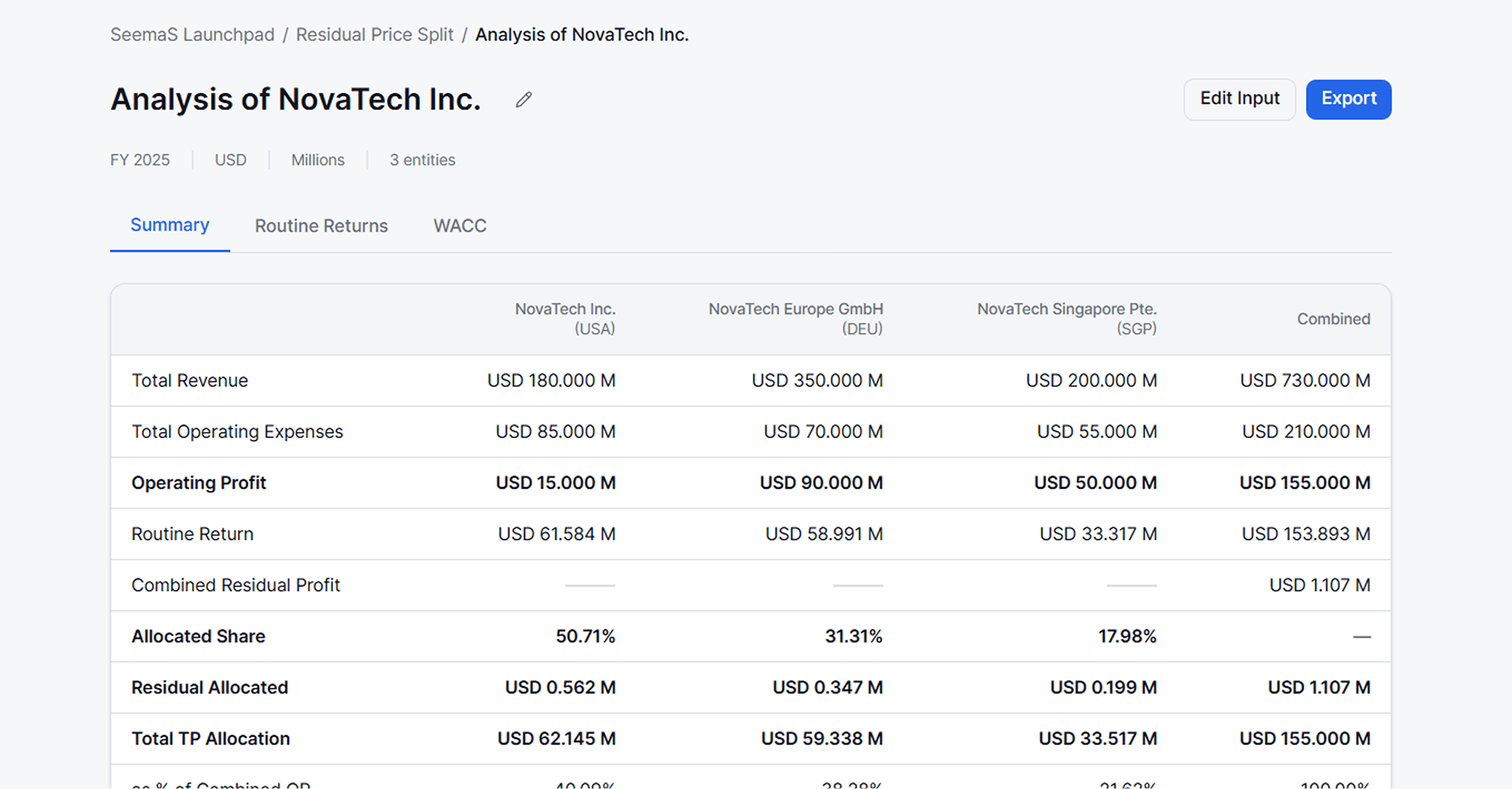

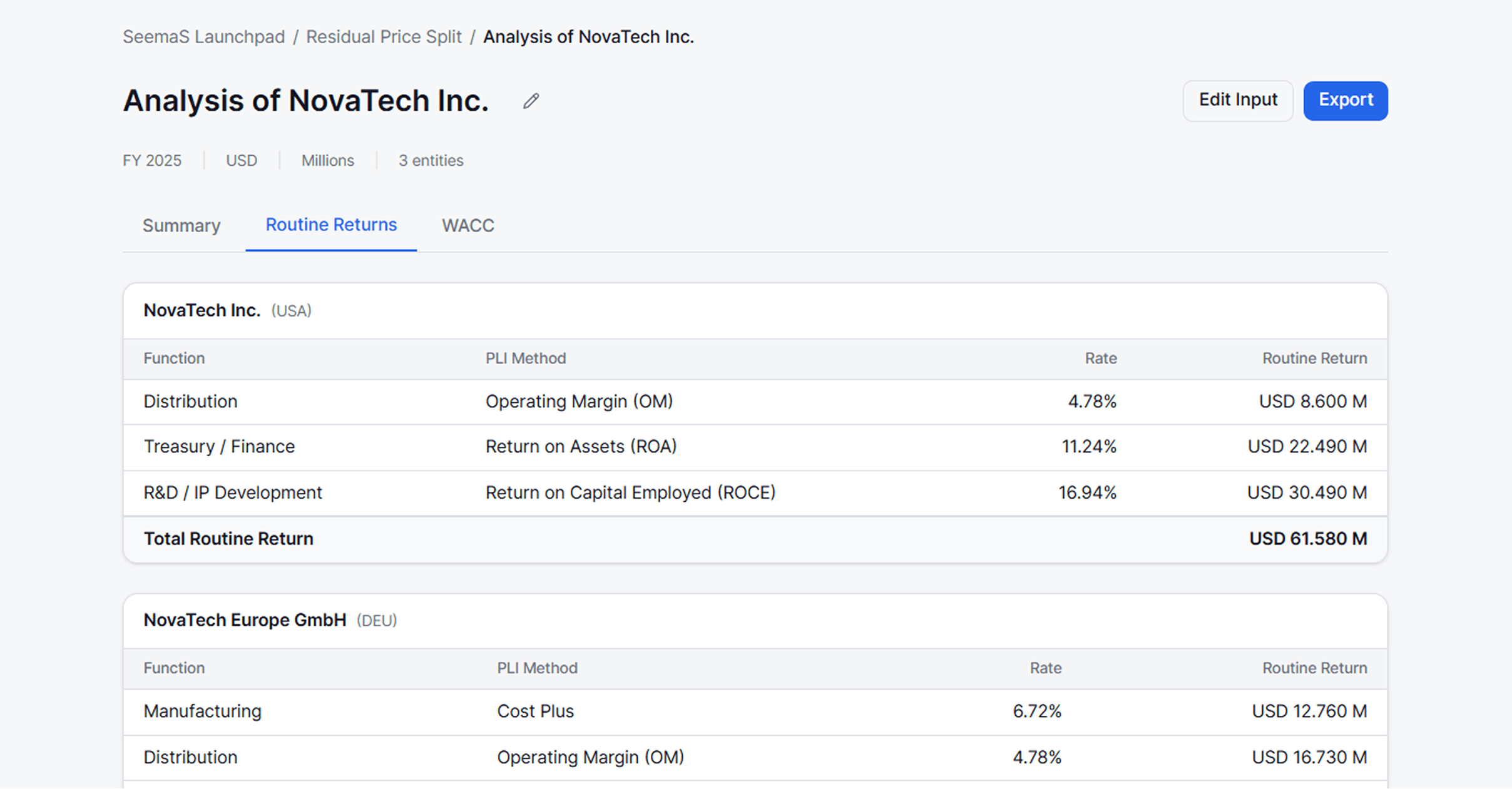

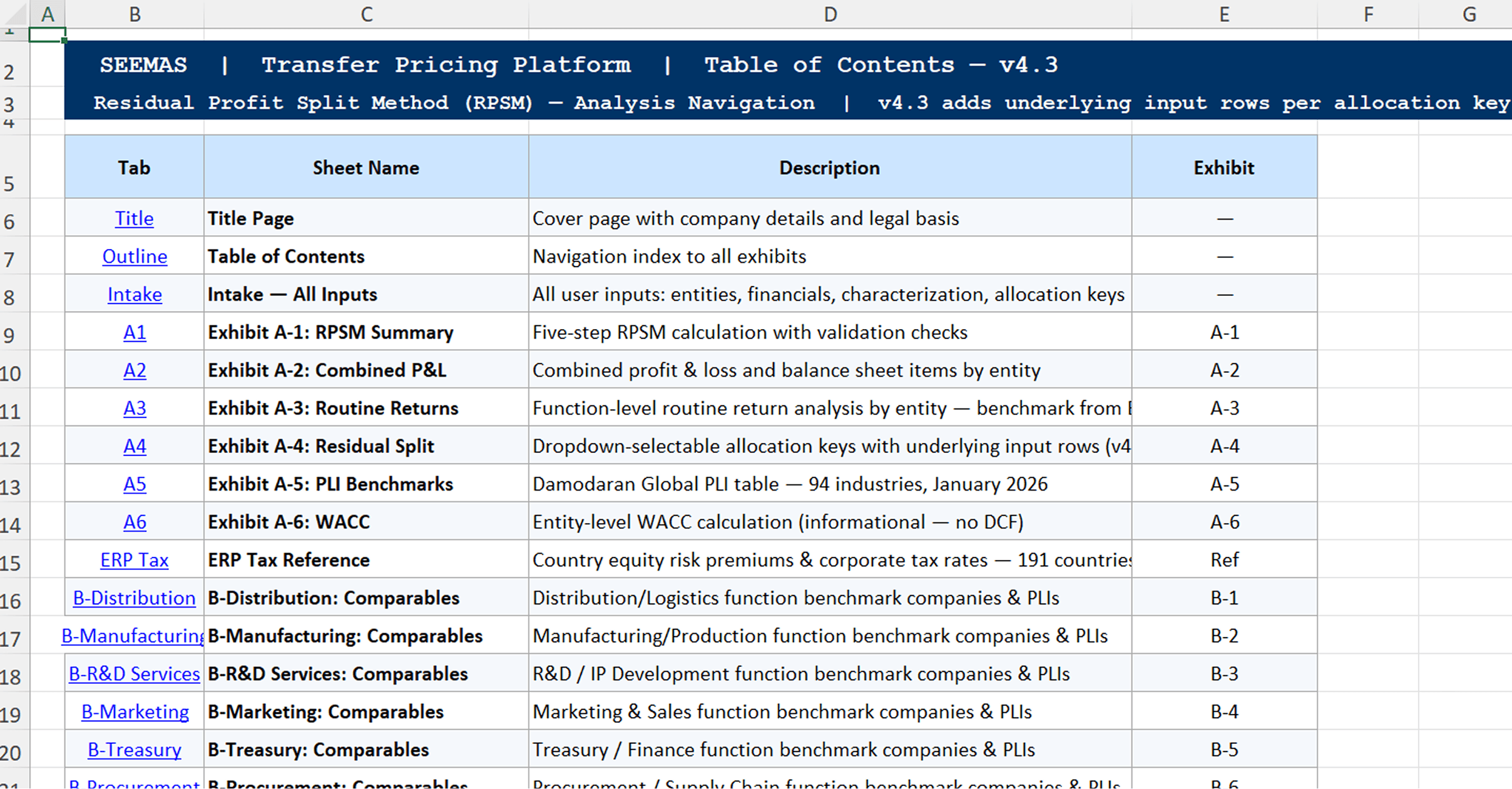

Routine Returns, Fully Benchmarked

Apply CPM and TNMM to each party’s routine functions before splitting residuals — so the foundation of the analysis is grounded in independent comparables.

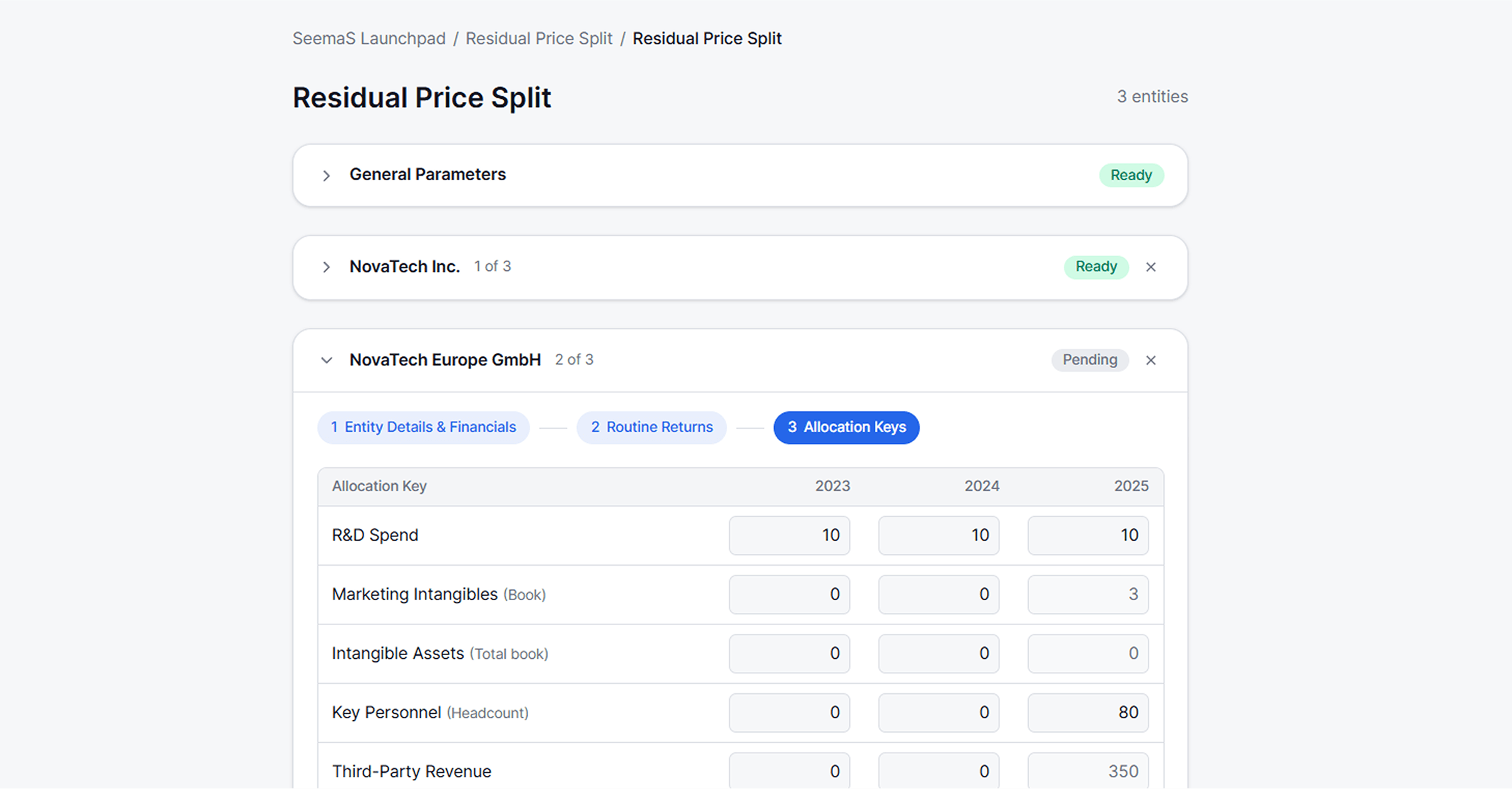

Allocation Keys with Substance

Tie residual splits to measurable value drivers (R&D spend, marketing intensity, DEMPE contributions) — not subjective weightings.

When Other Methods Fall Short

Document why CUP, resale price, cost-plus, and one-sided methods are not the best method — meeting the higher evidentiary bar OECD and IRS apply to profit splits.

Meet the TP Atlas

TP Atlas is the transfer pricing intelligence layer. It monitors regulatory updates across jurisdictions, flags documentation gaps, and answers your team's questions — so you spend less time researching and more time advising.